" height="232.354px" id="Kl9gPwrAr" transform="translate(1717.49 0)" width="75.42000000000007px"/><path d="M 73.28 0 C 113.58 0 134.65 28.09 134.65 68.088 L 134.65 77.554 L 25.34 77.554 C 25.34 117.55 46.71 144.726 81.22 144.726 C 104.12 144.726 118.47 133.428 129.76 118.466 L 134.95 121.215 C 127.63 148.389 105.03 167.929 70.83 167.929 C 26.26 167.929 0 132.817 0 89.155 C 0 35.724 31.14 0 73.28 0 Z M 68.7 14.961 C 44.58 14.961 29.01 37.556 26.56 62.898 L 106.56 62.898 C 106.56 33.587 93.73 14.961 68.7 14.961 Z" fill="rgb(0, 4, 26)" height="167.9295px" id="Dh1gctGLU" transform="translate(1575.69 67.478)" width="134.95000000000005px"/><path d="M 73.28 0 C 113.58 0 134.65 28.09 134.65 68.088 L 134.65 77.554 L 25.34 77.554 C 25.34 117.55 46.71 144.726 81.22 144.726 C 104.11 144.726 118.46 133.428 129.76 118.466 L 134.95 121.215 C 127.62 148.389 105.03 167.929 70.83 167.929 C 26.26 167.929 0 132.817 0 89.155 C 0 35.724 31.14 0 73.28 0 Z M 68.7 14.961 C 44.58 14.961 29 37.556 26.56 62.898 L 106.56 62.898 C 106.56 33.587 93.73 14.961 68.7 14.961 Z" fill="rgb(0, 4, 26)" height="167.9295px" id="sTkc1lbds" transform="translate(1429.94 67.478)" width="134.95000000000005px"/><path d="M 51.9 0 L 51.9 97.399 C 66.87 82.744 84.88 67.477 110.22 67.477 C 136.79 67.477 152.97 81.828 152.97 117.551 L 152.97 204.264 C 152.97 218.309 163.04 219.836 176.78 221.668 L 176.78 232.354 L 101.37 232.354 L 101.37 221.668 C 114.8 219.836 124.88 218.309 124.88 204.264 L 124.88 119.688 C 124.88 97.705 116.02 90.072 96.48 90.072 C 80.61 90.072 63.81 97.094 51.9 106.254 L 51.9 204.264 C 51.9 218.309 61.98 219.836 75.41 221.668 L 75.41 232.354 L 0 232.354 L 0 221.668 C 13.74 219.836 23.81 218.309 23.81 204.264 L 23.81 32.365 L 1.53 21.678 L 1.53 15.266 L 44.27 0 Z" fill="rgb(0, 4, 26)" height="232.354px" id="u4ObJrh1g" transform="translate(1248.66 0)" width="176.77999999999997px"/><path d="M 168.84 119.994 L 201.21 29.922 C 202.43 26.258 203.04 24.121 203.04 21.678 C 203.04 14.35 197.24 12.824 181.67 10.687 L 181.67 0 L 239.07 0 L 239.07 10.687 C 225.33 15.572 223.8 16.182 221.36 22.9 L 168.23 164.877 L 160.6 164.877 L 120.3 57.096 L 79.38 164.877 L 72.06 164.877 L 17.4 22.9 C 14.96 16.182 13.43 15.266 0 10.687 L 0 0 L 69 0 L 69 10.687 C 53.74 12.824 47.63 14.35 47.63 21.678 C 47.63 24.121 48.55 27.48 49.77 30.838 L 82.13 119.383 L 112.36 37.555 L 107.17 22.9 C 104.73 16.182 102.89 15.266 89.15 10.687 L 89.15 0 L 157.24 0 L 157.24 10.687 C 141.36 12.824 135.56 14.35 135.56 21.678 C 135.56 24.121 136.48 27.48 137.7 30.838 Z" fill="rgb(0, 4, 26)" height="164.8768px" id="BakTvJk8x" transform="translate(1013.56 70.533)" width="239.07000000000016px"/><path d="M 124.879 136.786 L 124.879 52.21 C 124.879 30.227 116.025 22.594 96.484 22.594 C 80.607 22.594 63.203 29.617 51.601 38.776 L 51.601 136.786 C 51.601 150.832 61.371 152.358 75.111 154.191 L 75.111 164.876 L 0 164.876 L 0 154.191 C 13.435 152.358 23.511 150.832 23.511 136.786 L 23.511 32.365 L 1.527 21.678 L 1.527 15.266 L 43.968 0 L 51.601 0 L 51.601 29.922 C 66.562 15.266 84.881 0 110.224 0 C 136.787 0 152.969 14.35 152.969 50.074 L 152.969 136.786 C 152.969 150.832 163.048 152.358 176.788 154.191 L 176.788 164.876 L 101.369 164.876 L 101.369 154.191 C 114.803 152.358 124.879 150.832 124.879 136.786 Z" fill="rgb(0, 4, 26)" height="164.8765px" id="KLM9nuer9" transform="translate(846.002 67.478)" width="176.788px"/><path d="M 36.333 40.914 C 25.342 40.914 16.487 31.754 16.487 20.457 C 16.487 9.16 25.342 0 36.333 0 C 47.325 0 56.18 9.16 56.18 20.457 C 56.18 31.754 47.325 40.914 36.333 40.914 Z M 51.6 62.592 L 51.6 199.379 C 51.6 213.424 61.37 214.951 75.11 216.783 L 75.11 227.469 L 0 227.469 L 0 216.783 C 13.434 214.951 23.51 213.424 23.51 199.379 L 23.51 94.957 L 1.526 84.27 L 1.526 77.858 L 43.967 62.592 Z" fill="rgb(0, 4, 26)" height="227.46875000000003px" id="wc5drELYV" transform="translate(763.165 4.885)" width="75.11000000000001px"/><path d="M 51.905 151.137 L 51.905 196.937 C 51.905 210.981 61.981 212.507 75.721 214.339 L 75.721 225.026 L 0 225.026 L 0 214.339 C 13.739 212.507 23.815 210.981 23.815 196.937 L 23.815 32.365 L 1.526 21.678 L 1.526 15.266 L 44.577 0 L 51.905 0 L 51.905 26.564 C 64.729 10.381 81.522 0 104.116 0 C 145.641 0 167.319 34.197 167.319 76.332 C 167.319 132.817 132.206 167.929 91.903 167.929 C 72.973 167.929 58.622 160.907 51.905 151.137 Z M 91.292 153.885 C 119.688 153.885 139.229 128.542 139.229 89.155 C 139.229 54.654 125.794 20.457 91.598 20.457 C 76.637 20.457 61.065 25.648 51.905 35.418 L 51.905 111.445 C 51.905 139.535 67.477 153.885 91.292 153.885 Z" fill="rgb(0, 4, 26)" height="225.0265px" id="hvXNnfhq3" transform="translate(586.583 67.478)" width="167.31900000000007px"/><path d="M 68.698 220.446 C 39.997 220.446 15.571 210.676 2.137 199.379 L 0 149.305 L 10.686 149.305 C 19.846 181.364 38.471 205.18 69.614 205.18 C 98.315 205.18 115.719 191.135 115.719 166.098 C 115.719 145.03 101.979 135.26 65.034 121.52 C 24.426 106.559 2.442 91.903 2.442 57.402 C 2.442 25.037 26.563 0 69.309 0 C 94.04 0 116.329 8.244 132.817 19.236 L 132.817 65.951 L 122.741 65.951 C 115.719 36.334 97.399 15.266 67.782 15.266 C 42.135 15.266 29.006 29.922 29.006 49.463 C 29.006 70.225 39.387 79.69 77.247 93.735 C 122.13 110.223 143.503 126.1 143.503 159.991 C 143.503 199.073 109.307 220.446 68.698 220.446 Z" fill="rgb(0, 4, 26)" height="220.446px" id="LeoVvyEWA" transform="translate(437.081 14.96)" width="143.50299999999993px"/><path d="M 285.399 142.7 C 285.399 221.511 221.51 285.4 142.7 285.4 C 63.889 285.4 0 221.512 0 142.701 C 0 63.89 63.889 0 142.7 0 C 144.941 0 147.17 0.053 149.386 0.155 C 90.503 20.747 48.267 76.791 48.267 142.7 L 48.274 143.921 C 48.928 195.512 90.953 237.133 142.699 237.133 C 194.853 237.133 237.132 194.854 237.132 142.7 C 237.132 105.427 215.539 73.207 184.189 57.849 C 189.074 56.989 194.102 56.54 199.238 56.54 C 219.055 56.54 237.299 63.225 251.854 74.465 C 272.265 90.229 285.399 114.93 285.399 142.7 Z" fill="rgb(0, 4, 26)" height="285.39957000000004px" id="KzUAEFh67" transform="translate(0 3.169)" width="285.399px"/><path d="M 237.132 142.7 C 237.132 112.259 222.723 85.181 200.371 67.919 C 184.419 55.599 164.409 48.268 142.699 48.268 C 131.832 48.268 121.385 50.105 111.658 53.489 C 74.759 66.328 48.267 101.415 48.267 142.7 C 48.267 179.971 69.857 212.191 101.205 227.55 C 96.32 228.411 91.292 228.861 86.16 228.861 C 38.576 228.86 0.001 190.286 0 142.701 L 0.011 140.857 C 0.999 62.896 64.505 0 142.7 0 C 221.51 0 285.399 63.89 285.399 142.701 C 285.399 221.511 221.51 285.4 142.7 285.4 C 140.459 285.4 138.231 285.347 136.016 285.244 C 194.897 264.652 237.132 208.609 237.132 142.7 Z" fill="rgb(0, 4, 26)" height="285.39957000000004px" id="toapGQ6m3" transform="translate(56.539 3.169)" width="285.3991px"/></svg>)

" height="285.4px" id="ccL2W0i9_" width="285.399px"/><path d="M 237.132 142.7 C 237.132 112.259 222.723 85.181 200.371 67.919 C 184.419 55.599 164.409 48.268 142.699 48.268 C 131.832 48.268 121.385 50.105 111.658 53.489 C 74.759 66.328 48.267 101.415 48.267 142.7 C 48.267 179.971 69.857 212.191 101.205 227.55 C 96.32 228.41 91.292 228.86 86.16 228.86 C 38.576 228.86 0.001 190.285 0 142.701 L 0.011 140.857 C 0.999 62.896 64.505 0 142.7 0 C 221.51 0 285.399 63.89 285.399 142.701 C 285.399 221.511 221.51 285.4 142.7 285.4 C 140.459 285.4 138.231 285.346 136.016 285.244 C 194.897 264.652 237.132 208.608 237.132 142.7 Z" fill="rgb(0, 4, 26)" height="285.4px" id="jBpX3TwPH" transform="translate(56.539 0)" width="285.3991px"/></svg>)

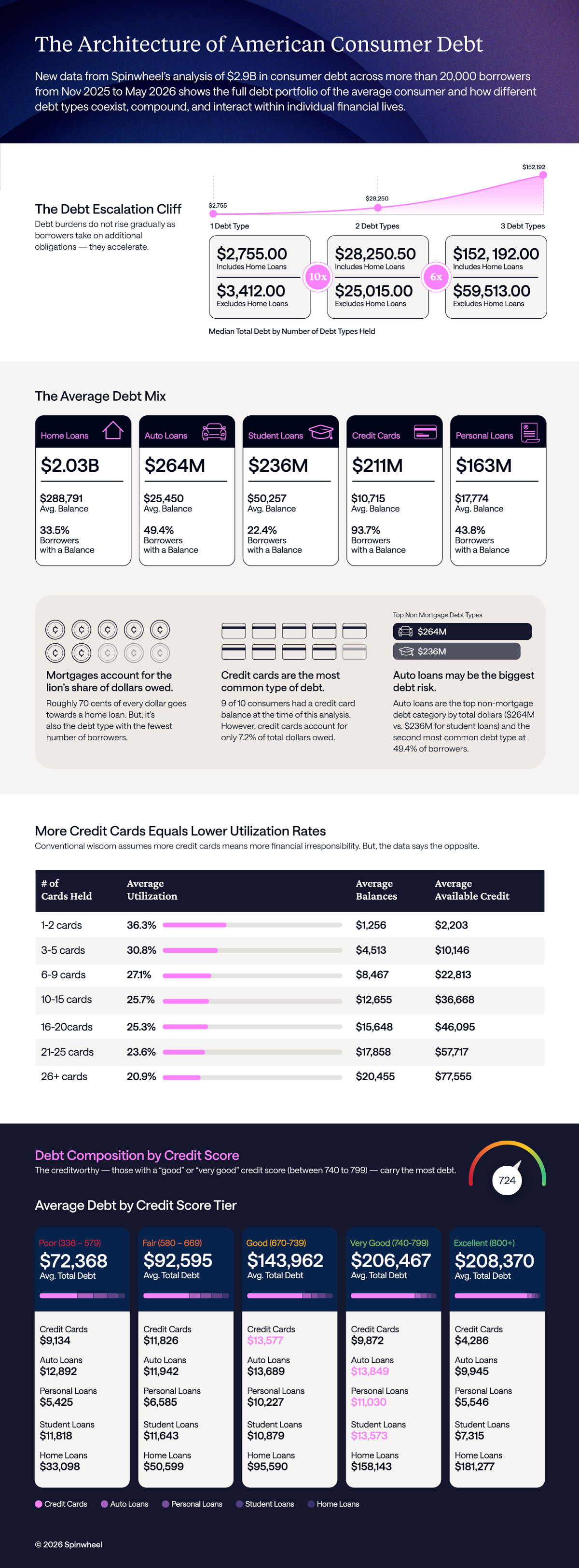

Americans are carrying record-setting debt levels. Federal Reserve Bank of New York data shows household debt reached $18.8 trillion at the end of 2025, with balances rising across nearly every major category.

But Spinwheel’s data suggests the real inflection point may not be how much consumers owe within a single liability. The real warning sign of financial stress may be complexity. Debt burdens do not rise gradually as borrowers take on additional obligations — they accelerate. More credit cards doesn’t mean higher balances across the board. And, the biggest debt burden (not including mortgages) for many consumers isn’t what you’d expect.

New data from Spinwheel’s analysis of $2.9B in consumer debt across more than 20,000 borrowers from Nov 2025 to May 2026 shows the full debt portfolio of the average consumer and how different debt types coexist, compound, and interact within individual financial lives.

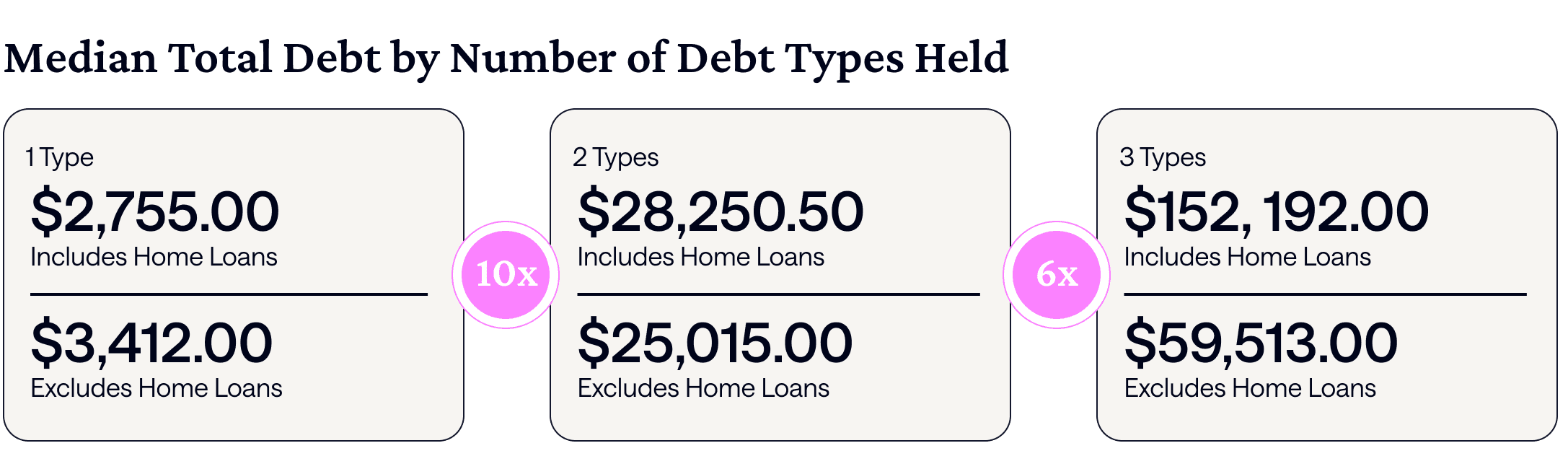

The Debt Escalation Cliff

The most striking finding in the data is not about any single debt type. It's about what happens when borrowers add a second one.

When consumers move from one debt type to two types of debt, the median debt balance increases by more than 10 times — from $2,755 to $28,250.50. The jump from 2 debt types to 3 is equally dramatic. Median debt balances are more than 6 times higher. This is likely driven heavily by home loans.

However, even if you exclude home loans, total balances are still 7.3 times higher when a second debt type enters the picture.

This isn't additive. It's multiplicative. Crossing into multiple debt categories appears to fundamentally change a borrower’s financial profile.

A second debt obligation signals a borrower whose financial commitments have expanded into multiple dimensions. The single most predictive signal for total debt burden is the number of debt types being managed simultaneously.

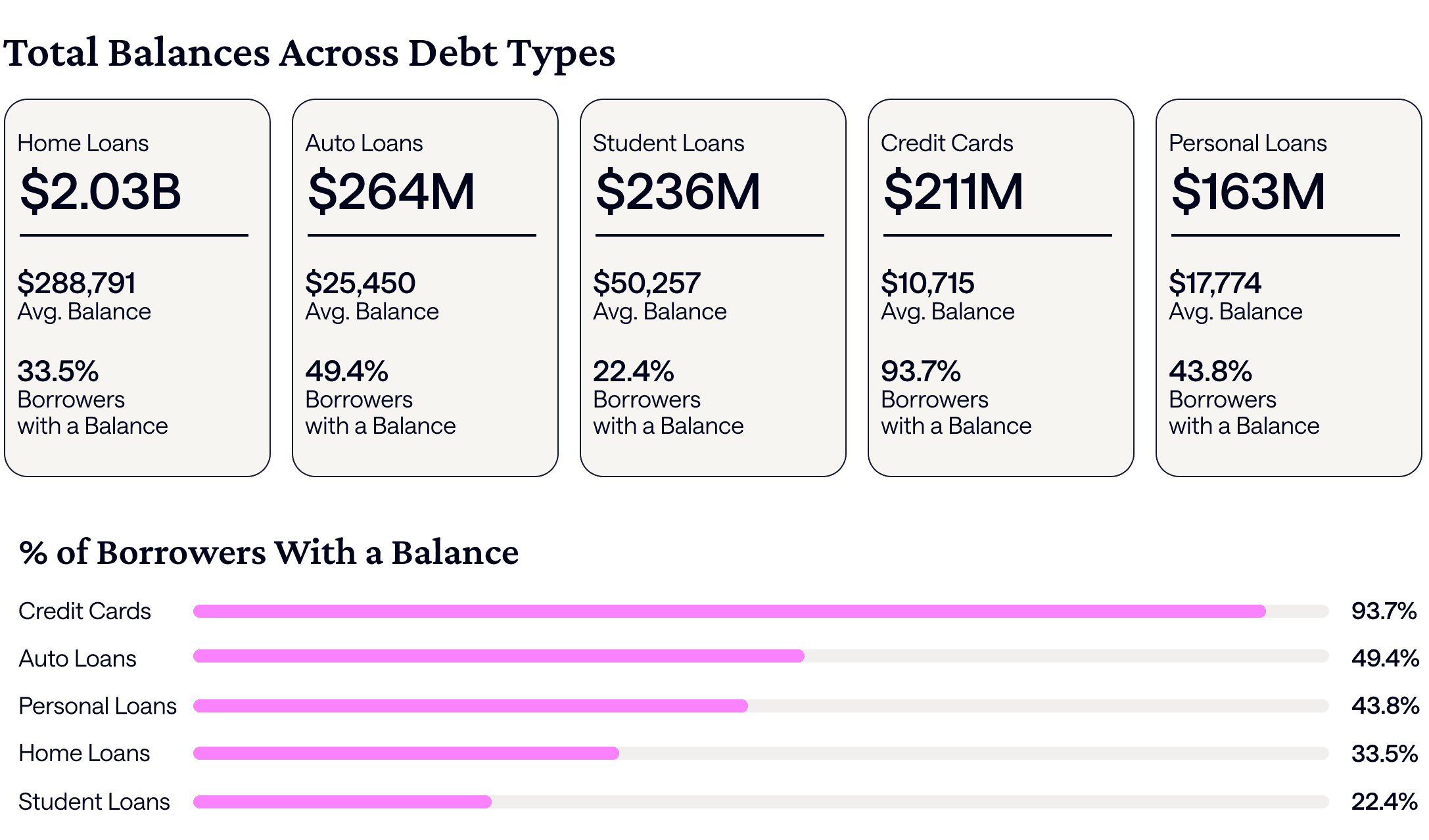

The Average Debt Mix

Perhaps unsurprisingly, mortgages account for the lion’s share of dollars owed by consumers. In fact, roughly 70 cents of every dollar goes towards a home loan. But, it’s also the debt type with the fewest number of borrowers.

By comparison, the most common type of debt is credit cards. Nine out of 10 consumers had a credit card balance at the time of this analysis. However, credit cards account for only 7.2% of total dollars owed.

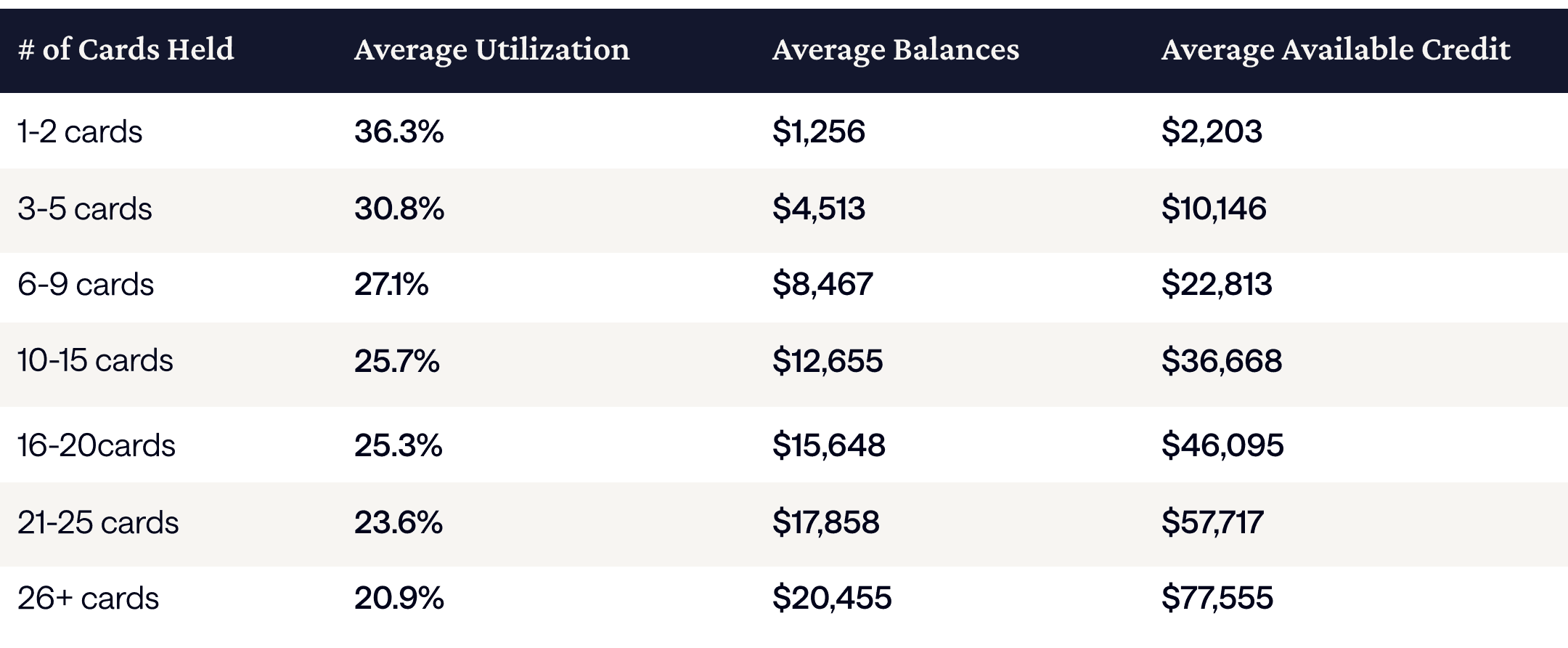

More Credit Cards Equals Lower Utilization Rates

For most consumers, credit cards are simply a way of life. Most consumers carry one or more credit cards in a state of revolving-debt maintenance. But, Spinwheel’s data shows credit utilization rates change as consumers acquire more credit cards.

Conventional wisdom assumes more credit cards means more financial irresponsibility. But, the data says the opposite.

Consumers that hold more than 25 credit cards only utilize 20.9% of their available credit limits, compared to those with just 1 to 2 credit cards. Among this group (1 to 2 cards), consumers use an average 36.3% of their available credit.

This likely reflects a financially sophisticated subpopulation of consumers who are optimizing for rewards, taking advantage of low interest rates by opening new cards, and building credit by holding cards they don’t actively use.

Of course, high card counts alone do not guarantee financial stability. But within this dataset, larger card portfolios correlate with lower utilization rates rather than elevated borrowing pressure.

(Fun fact: Spinwheel’s data set shows one borrower with 170 different credit cards! For this outlier, the average utilization rate was 57.9% — showing there is indeed such a thing as too many cards.)

Intentional or not, having more cards is likely a credit-building strategy, not a symptom of distress. The U.S. credit system rewards this behavior unconditionally.

The Potential Debt Crisis Nobody Talks About

While most headlines focus on student and personal loans as a big driver of debt, they make up the smallest shares of debt in the United States. Aside from mortgages, our data shows a different debt type leading the way — both in share of all debt and total balances.

Auto loans are the top non-mortgage debt category by total dollars ($264M vs. $236M for student loans) and the second most common debt type at 49.4% of borrowers. And, unlike mortgages, auto loans are tied to a depreciating asset. The car, not the diploma, anchors American consumer debt.

Nearly half of consumers have auto loans with balances, surpassing student loan debt by more than double. The median auto payment is $582 per month — consuming 9.5% of the U.S. median household income with a single monthly car payment. This means the far larger and less visible crisis may be that Americans are systematically over-leveraged on depreciating assets.

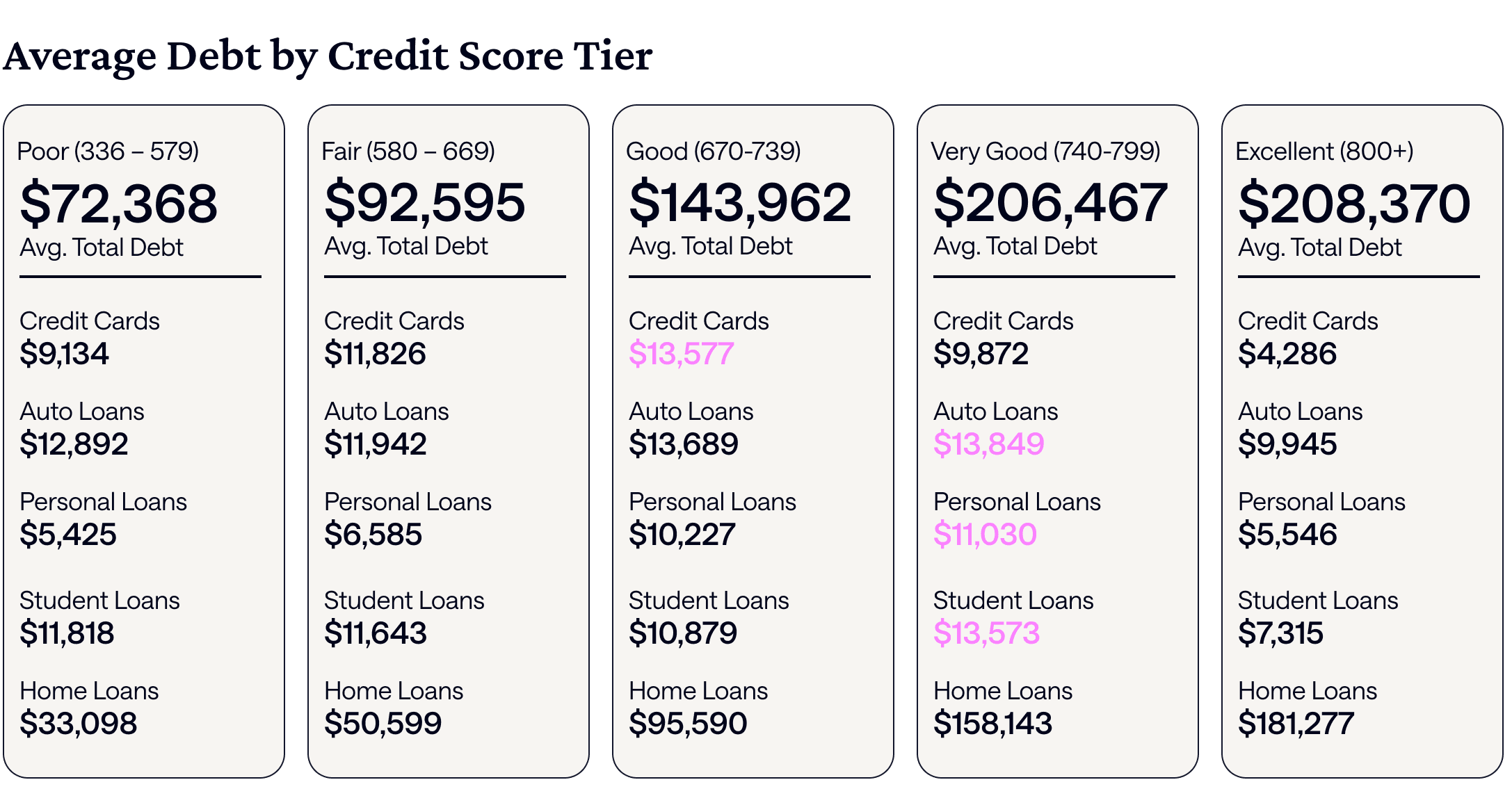

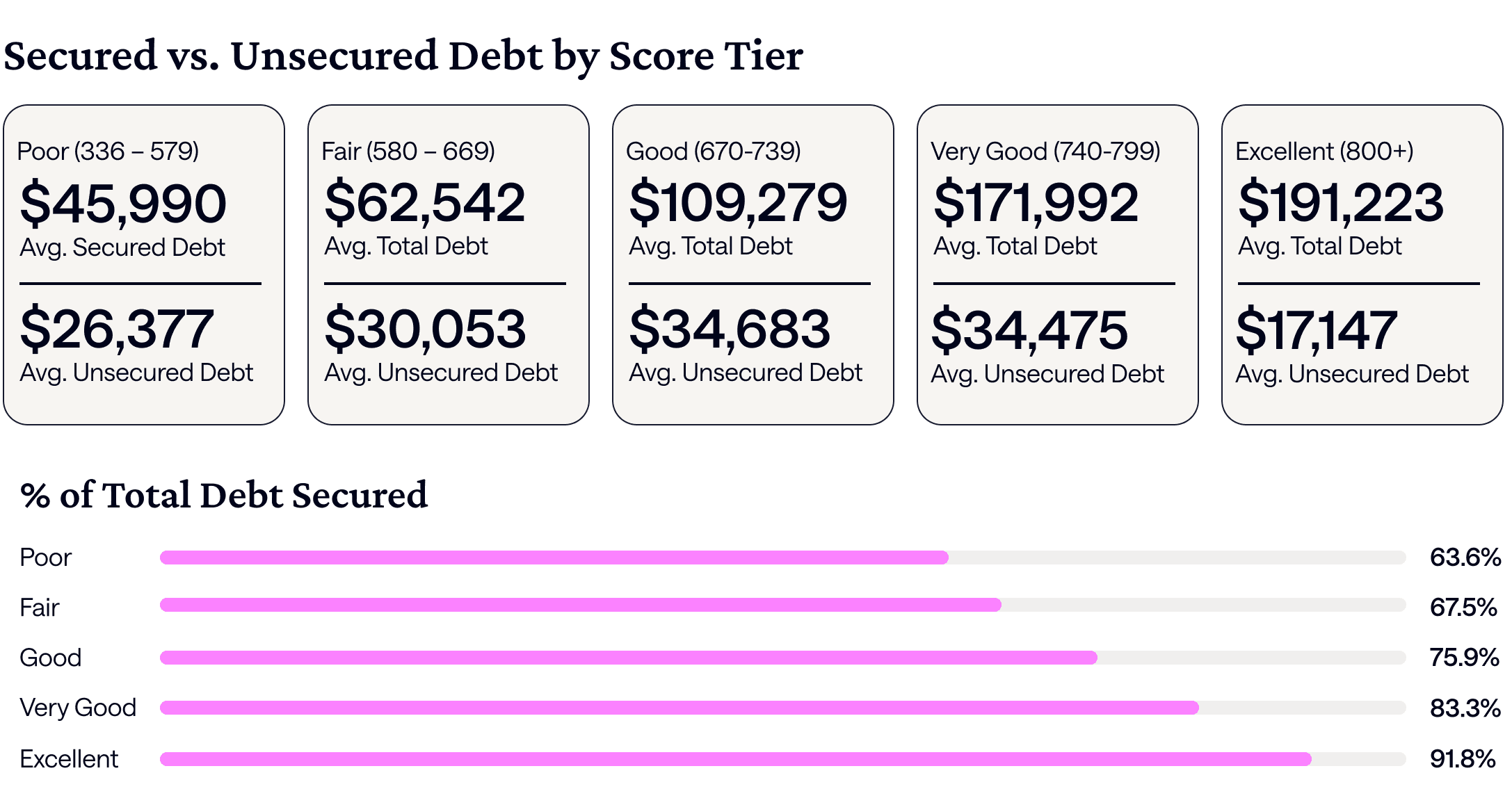

Debt Composition by Credit Score

Looking at the average total debt across consumers, the average total debt grows steadily as credit scores improve — better access to credit means higher overall average debt balances. But, looking into the types of debt by credit score paints an interesting picture.

The Creditworthy Middle

Those with a “good” credit score (between 670 to 739) carry more credit card debt than any other group while those with “very good” credit scores (between 740 to 799) carry the most average debt across personal loans and student loans.

Why? These borrowers likely occupy a financially precarious middle ground: creditworthy enough to access large amounts of debt, but leveraged enough to prevent their scores from moving into the highest tier.

Excellent Scores Drive Less Unsecured Debt

Among those with the highest credit scores, the data shows borrowers with the best credit scores carry less unsecured debt — those with “excellent” scores have the lowest average credit card and student loan balances of any tier.

The single biggest blind spot in an averages-only analysis of total debt is mixing different types of balance sheets. For instance, a $200K mortgage is completely different from $200K in credit card debt.

Bottom line: high-score borrowers carry more dollars but a much healthier mix. Secured balances grow by more than 4 times from borrowers with “poor” credit scores to “excellent” scores.

The Good and Bad of Credit

Debt itself is not inherently unhealthy. Modern financial life depends on it. The issue is that consumers are increasingly layering multiple forms of debt simultaneously — often within a credit system designed to evaluate accounts individually rather than holistically.

What once looked like a single monthly obligation has become a layered financial ecosystem of credit cards, auto loans, personal loans, installment plans, and revolving balances interacting simultaneously. As borrowers accumulate more debt types, financial pressure compounds faster than traditional metrics can capture.

That has major implications for how financial health is measured.

A credit score can indicate repayment consistency while masking rising obligations elsewhere. A borrower with 10 credit cards may actually be financially stable, while a borrower with only 1 credit card may already be approaching financial distress. Even the largest debt burdens are no longer concentrated where many institutions assume they are.

The result is a consumer credit system that often measures payment behavior more effectively than financial resilience. For lenders and fintechs, that means the next generation of underwriting and financial wellness tools cannot rely solely on isolated balances, utilization ratios, or credit scores.

As debt spreads across more products, providers, and repayment systems, financial visibility becomes increasingly fragmented for both consumers and institutions.

Understanding a consumer’s full debt profile — including how debt overlaps and how obligations compound once consumers move beyond a single debt type — may become one of the most important indicators of long-term financial risk.

This is because the clearest signal of financial strain is no longer how much debt consumers carry. It’s how many financial systems they’re trying to manage at once.

Jessica Kendall

Head of Content and Comms

{kind=link}