" height="232.354px" id="Kl9gPwrAr" transform="translate(1717.49 0)" width="75.42000000000007px"/><path d="M 73.28 0 C 113.58 0 134.65 28.09 134.65 68.088 L 134.65 77.554 L 25.34 77.554 C 25.34 117.55 46.71 144.726 81.22 144.726 C 104.12 144.726 118.47 133.428 129.76 118.466 L 134.95 121.215 C 127.63 148.389 105.03 167.929 70.83 167.929 C 26.26 167.929 0 132.817 0 89.155 C 0 35.724 31.14 0 73.28 0 Z M 68.7 14.961 C 44.58 14.961 29.01 37.556 26.56 62.898 L 106.56 62.898 C 106.56 33.587 93.73 14.961 68.7 14.961 Z" fill="rgb(0, 4, 26)" height="167.9295px" id="Dh1gctGLU" transform="translate(1575.69 67.478)" width="134.95000000000005px"/><path d="M 73.28 0 C 113.58 0 134.65 28.09 134.65 68.088 L 134.65 77.554 L 25.34 77.554 C 25.34 117.55 46.71 144.726 81.22 144.726 C 104.11 144.726 118.46 133.428 129.76 118.466 L 134.95 121.215 C 127.62 148.389 105.03 167.929 70.83 167.929 C 26.26 167.929 0 132.817 0 89.155 C 0 35.724 31.14 0 73.28 0 Z M 68.7 14.961 C 44.58 14.961 29 37.556 26.56 62.898 L 106.56 62.898 C 106.56 33.587 93.73 14.961 68.7 14.961 Z" fill="rgb(0, 4, 26)" height="167.9295px" id="sTkc1lbds" transform="translate(1429.94 67.478)" width="134.95000000000005px"/><path d="M 51.9 0 L 51.9 97.399 C 66.87 82.744 84.88 67.477 110.22 67.477 C 136.79 67.477 152.97 81.828 152.97 117.551 L 152.97 204.264 C 152.97 218.309 163.04 219.836 176.78 221.668 L 176.78 232.354 L 101.37 232.354 L 101.37 221.668 C 114.8 219.836 124.88 218.309 124.88 204.264 L 124.88 119.688 C 124.88 97.705 116.02 90.072 96.48 90.072 C 80.61 90.072 63.81 97.094 51.9 106.254 L 51.9 204.264 C 51.9 218.309 61.98 219.836 75.41 221.668 L 75.41 232.354 L 0 232.354 L 0 221.668 C 13.74 219.836 23.81 218.309 23.81 204.264 L 23.81 32.365 L 1.53 21.678 L 1.53 15.266 L 44.27 0 Z" fill="rgb(0, 4, 26)" height="232.354px" id="u4ObJrh1g" transform="translate(1248.66 0)" width="176.77999999999997px"/><path d="M 168.84 119.994 L 201.21 29.922 C 202.43 26.258 203.04 24.121 203.04 21.678 C 203.04 14.35 197.24 12.824 181.67 10.687 L 181.67 0 L 239.07 0 L 239.07 10.687 C 225.33 15.572 223.8 16.182 221.36 22.9 L 168.23 164.877 L 160.6 164.877 L 120.3 57.096 L 79.38 164.877 L 72.06 164.877 L 17.4 22.9 C 14.96 16.182 13.43 15.266 0 10.687 L 0 0 L 69 0 L 69 10.687 C 53.74 12.824 47.63 14.35 47.63 21.678 C 47.63 24.121 48.55 27.48 49.77 30.838 L 82.13 119.383 L 112.36 37.555 L 107.17 22.9 C 104.73 16.182 102.89 15.266 89.15 10.687 L 89.15 0 L 157.24 0 L 157.24 10.687 C 141.36 12.824 135.56 14.35 135.56 21.678 C 135.56 24.121 136.48 27.48 137.7 30.838 Z" fill="rgb(0, 4, 26)" height="164.8768px" id="BakTvJk8x" transform="translate(1013.56 70.533)" width="239.07000000000016px"/><path d="M 124.879 136.786 L 124.879 52.21 C 124.879 30.227 116.025 22.594 96.484 22.594 C 80.607 22.594 63.203 29.617 51.601 38.776 L 51.601 136.786 C 51.601 150.832 61.371 152.358 75.111 154.191 L 75.111 164.876 L 0 164.876 L 0 154.191 C 13.435 152.358 23.511 150.832 23.511 136.786 L 23.511 32.365 L 1.527 21.678 L 1.527 15.266 L 43.968 0 L 51.601 0 L 51.601 29.922 C 66.562 15.266 84.881 0 110.224 0 C 136.787 0 152.969 14.35 152.969 50.074 L 152.969 136.786 C 152.969 150.832 163.048 152.358 176.788 154.191 L 176.788 164.876 L 101.369 164.876 L 101.369 154.191 C 114.803 152.358 124.879 150.832 124.879 136.786 Z" fill="rgb(0, 4, 26)" height="164.8765px" id="KLM9nuer9" transform="translate(846.002 67.478)" width="176.788px"/><path d="M 36.333 40.914 C 25.342 40.914 16.487 31.754 16.487 20.457 C 16.487 9.16 25.342 0 36.333 0 C 47.325 0 56.18 9.16 56.18 20.457 C 56.18 31.754 47.325 40.914 36.333 40.914 Z M 51.6 62.592 L 51.6 199.379 C 51.6 213.424 61.37 214.951 75.11 216.783 L 75.11 227.469 L 0 227.469 L 0 216.783 C 13.434 214.951 23.51 213.424 23.51 199.379 L 23.51 94.957 L 1.526 84.27 L 1.526 77.858 L 43.967 62.592 Z" fill="rgb(0, 4, 26)" height="227.46875000000003px" id="wc5drELYV" transform="translate(763.165 4.885)" width="75.11000000000001px"/><path d="M 51.905 151.137 L 51.905 196.937 C 51.905 210.981 61.981 212.507 75.721 214.339 L 75.721 225.026 L 0 225.026 L 0 214.339 C 13.739 212.507 23.815 210.981 23.815 196.937 L 23.815 32.365 L 1.526 21.678 L 1.526 15.266 L 44.577 0 L 51.905 0 L 51.905 26.564 C 64.729 10.381 81.522 0 104.116 0 C 145.641 0 167.319 34.197 167.319 76.332 C 167.319 132.817 132.206 167.929 91.903 167.929 C 72.973 167.929 58.622 160.907 51.905 151.137 Z M 91.292 153.885 C 119.688 153.885 139.229 128.542 139.229 89.155 C 139.229 54.654 125.794 20.457 91.598 20.457 C 76.637 20.457 61.065 25.648 51.905 35.418 L 51.905 111.445 C 51.905 139.535 67.477 153.885 91.292 153.885 Z" fill="rgb(0, 4, 26)" height="225.0265px" id="hvXNnfhq3" transform="translate(586.583 67.478)" width="167.31900000000007px"/><path d="M 68.698 220.446 C 39.997 220.446 15.571 210.676 2.137 199.379 L 0 149.305 L 10.686 149.305 C 19.846 181.364 38.471 205.18 69.614 205.18 C 98.315 205.18 115.719 191.135 115.719 166.098 C 115.719 145.03 101.979 135.26 65.034 121.52 C 24.426 106.559 2.442 91.903 2.442 57.402 C 2.442 25.037 26.563 0 69.309 0 C 94.04 0 116.329 8.244 132.817 19.236 L 132.817 65.951 L 122.741 65.951 C 115.719 36.334 97.399 15.266 67.782 15.266 C 42.135 15.266 29.006 29.922 29.006 49.463 C 29.006 70.225 39.387 79.69 77.247 93.735 C 122.13 110.223 143.503 126.1 143.503 159.991 C 143.503 199.073 109.307 220.446 68.698 220.446 Z" fill="rgb(0, 4, 26)" height="220.446px" id="LeoVvyEWA" transform="translate(437.081 14.96)" width="143.50299999999993px"/><path d="M 285.399 142.7 C 285.399 221.511 221.51 285.4 142.7 285.4 C 63.889 285.4 0 221.512 0 142.701 C 0 63.89 63.889 0 142.7 0 C 144.941 0 147.17 0.053 149.386 0.155 C 90.503 20.747 48.267 76.791 48.267 142.7 L 48.274 143.921 C 48.928 195.512 90.953 237.133 142.699 237.133 C 194.853 237.133 237.132 194.854 237.132 142.7 C 237.132 105.427 215.539 73.207 184.189 57.849 C 189.074 56.989 194.102 56.54 199.238 56.54 C 219.055 56.54 237.299 63.225 251.854 74.465 C 272.265 90.229 285.399 114.93 285.399 142.7 Z" fill="rgb(0, 4, 26)" height="285.39957000000004px" id="KzUAEFh67" transform="translate(0 3.169)" width="285.399px"/><path d="M 237.132 142.7 C 237.132 112.259 222.723 85.181 200.371 67.919 C 184.419 55.599 164.409 48.268 142.699 48.268 C 131.832 48.268 121.385 50.105 111.658 53.489 C 74.759 66.328 48.267 101.415 48.267 142.7 C 48.267 179.971 69.857 212.191 101.205 227.55 C 96.32 228.411 91.292 228.861 86.16 228.861 C 38.576 228.86 0.001 190.286 0 142.701 L 0.011 140.857 C 0.999 62.896 64.505 0 142.7 0 C 221.51 0 285.399 63.89 285.399 142.701 C 285.399 221.511 221.51 285.4 142.7 285.4 C 140.459 285.4 138.231 285.347 136.016 285.244 C 194.897 264.652 237.132 208.609 237.132 142.7 Z" fill="rgb(0, 4, 26)" height="285.39957000000004px" id="toapGQ6m3" transform="translate(56.539 3.169)" width="285.3991px"/></svg>)

" height="285.4px" id="ccL2W0i9_" width="285.399px"/><path d="M 237.132 142.7 C 237.132 112.259 222.723 85.181 200.371 67.919 C 184.419 55.599 164.409 48.268 142.699 48.268 C 131.832 48.268 121.385 50.105 111.658 53.489 C 74.759 66.328 48.267 101.415 48.267 142.7 C 48.267 179.971 69.857 212.191 101.205 227.55 C 96.32 228.41 91.292 228.86 86.16 228.86 C 38.576 228.86 0.001 190.285 0 142.701 L 0.011 140.857 C 0.999 62.896 64.505 0 142.7 0 C 221.51 0 285.399 63.89 285.399 142.701 C 285.399 221.511 221.51 285.4 142.7 285.4 C 140.459 285.4 138.231 285.346 136.016 285.244 C 194.897 264.652 237.132 208.608 237.132 142.7 Z" fill="rgb(0, 4, 26)" height="285.4px" id="jBpX3TwPH" transform="translate(56.539 0)" width="285.3991px"/></svg>)

Debt is overwhelming.

That’s the consensus from the majority of consumers who participated in Spinwheel’s latest survey of more than 600 adult consumers.

While our previous Spin Signal report showed what happens when consumers move from one debt type to multiple debt types, this new research explores how consumers feel about debt, how they manage it, and what their responses reveal about the growing challenge of debt complexity.

Today's Debt Landscape Is More Complex Than Ever

Regardless of the amount or type of debt, 57% of consumers agree that thinking about debt is overwhelming. Among younger generations, this is even higher — 72% of Millennials and 74% of Gen Z consumers agree with this sentiment.

Feeling overwhelmed isn't driven by one specific debt product or one exceptionally large balance. It's a common experience across today's credit landscape, where consumers increasingly manage multiple financial relationships simultaneously.

To understand why debt feels so overwhelming, it's helpful to first understand what Americans actually owe. Every consumer who participated in this survey had some kind of debt with credit cards, mortgages, and auto loans leading the way.

The debt mix itself isn't the story. The story is what that mix creates. Most consumers are managing several different types of debt simultaneously, each with its own payment schedule, lender, interest rate, and digital experience.

Complexity compounds quickly. Taking it a step further, how this breaks down among different generations shows some interesting trendlines.

Debt Changes With Every Stage of Life

Unsurprisingly, younger generations have the most student loan debt as they are closer to college years. Likewise, Baby Boomers and Gen X hold more mortgages.

While these patterns largely reflect different life stages, they also illustrate how consumer credit becomes increasingly layered over time. Student loans often give way to auto loans, mortgages, credit cards, and eventually home equity products.

Rather than replacing one another, many of these obligations accumulate, creating more accounts, more payment schedules, and more opportunities for financial complexity. Gen X illustrates this dynamic most clearly.

The Debt Burdened Gen Xer

Among all generations, Gen X has the highest percentage of debt in every category except personal loans (beat only by Gen Z) and Buy Now, Pay Later (BNPL) balances. This high debt load is consistent with industry data.

For instance, Experian reports Gen Xers owe more than $158,000 on average, stating this is more than the balances of all other generations, and more than 50% higher than average debts of all consumers.

Why is this the case? Kiplinger points to the dual strain of a “sandwich generation” that is simultaneously supporting children longer into adulthood and taking care of aging parents. Rather than replacing old obligations, many Gen X households are carrying the financial responsibilities of multiple life stages simultaneously.

Creditworthy Household Income Levels

Life stage isn't the only factor influencing debt complexity. Household income also shapes how consumers borrow and the number of financial products they carry.

Our analysis shows those with household incomes of $120K or higher also have higher percentages of debt across nearly every debt type. The only exceptions are medical debt and student loans. This is likely a combination of increased creditworthiness to qualify for credit and lifestyle creep as households upgrade their lifestyle as income increases.

But, higher income doesn’t automatically mean they are more able to pay off debt. CBS News reported that delinquencies across all loan products for households earning more than $150,000 more than doubled from 2023 to 2024.

Understanding a Complete Consumer Debt Profile

The good news is that 9 in 10 consumers believe they have a clear picture of how much they owe, including credit card debt, loans, mortgages, and BNPL purchases. And, most (58%) don’t believe their credit score has ever prevented them from accessing a type of debt they want.

At first glance, consumers appear financially informed. Most feel confident about their overall debt picture. But confidence fades when the questions shift from knowing what they owe to understanding what to do about it.

When asked if they know the interest rates on their credit cards or loans without looking, nearly half (49%) said no. At the same time, nearly one-third of all respondents (31%) agree they want to consolidate their debt but don’t know how. And, for Gen Z respondents, 52% want to consolidate but aren’t sure how to do so.

More importantly, knowing what you owe and managing what you owe are not the same thing. Our research shows 28% of consumers agree they avoid looking at their finances when possible. This jumps to half among Gen Z consumers. Let that sink in: One out of every 2 Gen Z consumers avoids looking at their finances.

Why is Gen Z avoiding its finances? Several factors may contribute to this behavior. Gen Z entered adulthood during a period of elevated inflation, rising interest rates, and growing reliance on digital credit products like BNPL. At the same time, they are often managing financial relationships across multiple lenders, apps, and payment experiences.

When finances become fragmented, avoidance can become a coping mechanism rather than a sign of financial irresponsibility.

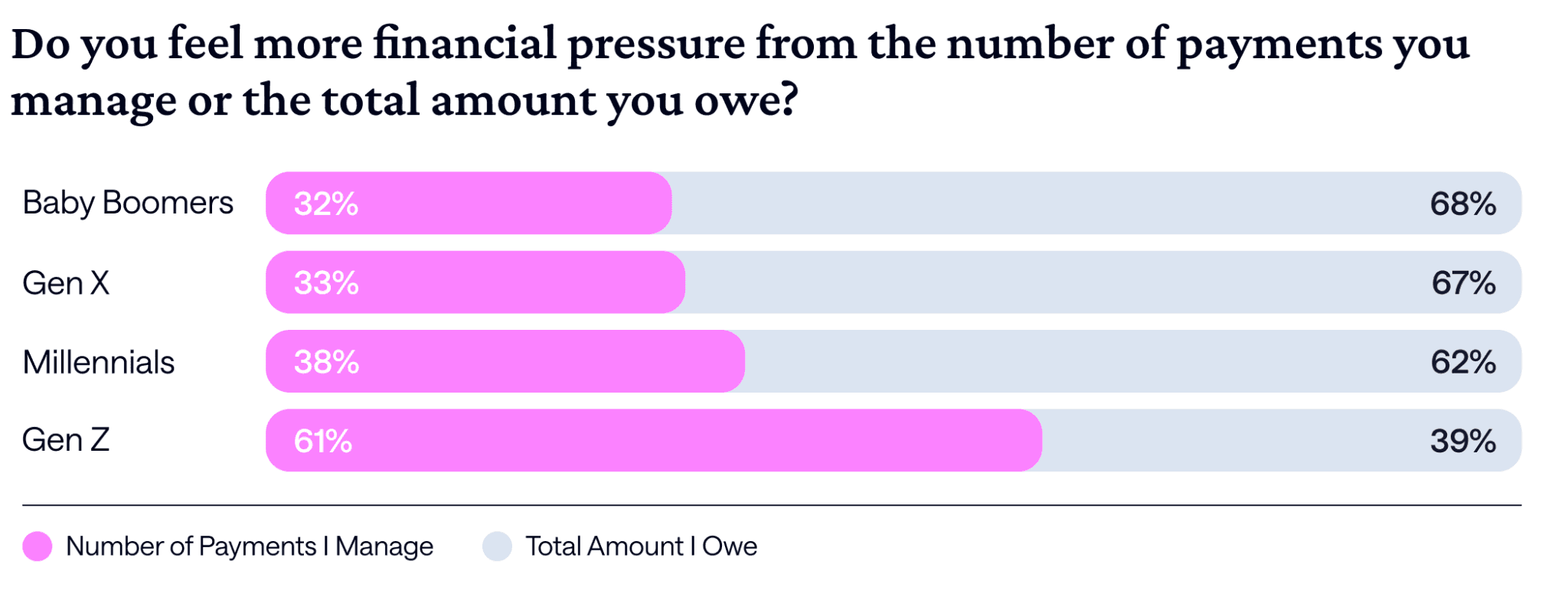

To add to this, Gen Z is also the only generation to say it feels more financial pressure based on the number of payments they manage instead of the total amount they owe. This points to an interesting shift in borrower perspectives. As debt accumulates, complexity is becoming a bigger pain point than simply dollars owed.

Together, these findings suggest that for younger consumers, financial stress is increasingly driven by coordination rather than calculation.

For lenders and financial institutions, this represents more than a financial wellness challenge. It is a product opportunity. Many consumers want less complexity.

Institutions that help customers understand what they owe, organize multiple obligations, identify opportunities to consolidate debt, or simplify repayment can build stronger engagement while improving customer outcomes.

Most Consumers Are Credit Creatures of Habit While Gen Z Is Breaking the Mold

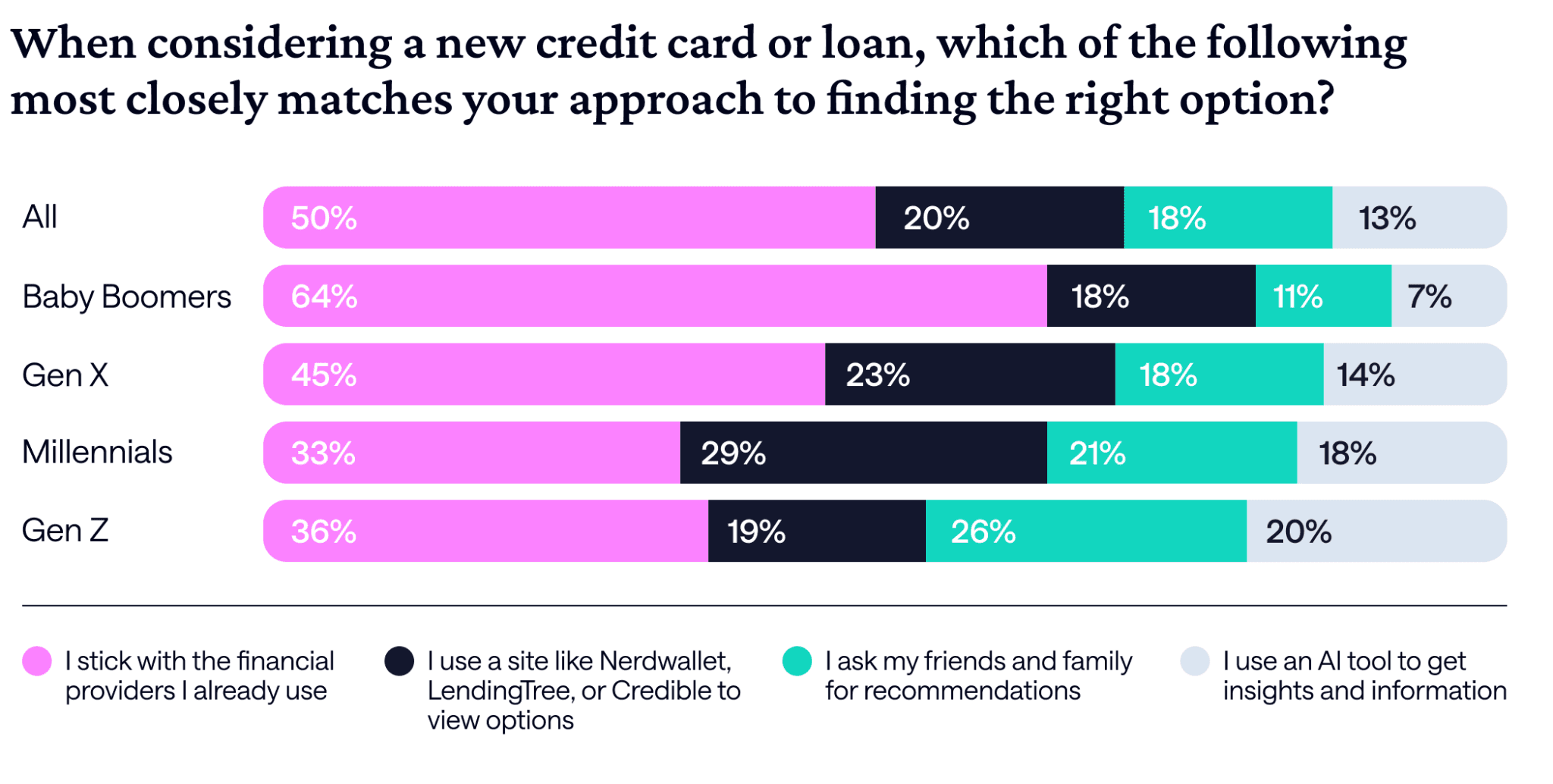

How do consumers choose which financial providers and lenders to use? Fifty percent of consumers say they stick with the financial providers they already use when considering a new credit card or loan. This is significant as financial institutions and fintechs continue to battle for primary financial relationships.

Every additional product deepens customer loyalty and increases lifetime value. Consumers who already trust an institution with their checking account or primary credit card often see less risk in opening additional credit products there.

Historically, this behavior has created a powerful competitive advantage for institutions that win primary financial relationships early. But, consumers as creatures of habit may be lessening among younger generations. Only 36% of Gen Z and 33% of Millennials say they stick with the providers they already use when considering new credit products.

Instead, Gen Z is becoming increasingly more likely to leverage AI for insights and information (20%) or ask their friends and family for recommendations (26%) compared to other generations. And, among Millennials, marketplace sites like NerdWallet are most popular when looking for the right option for a new credit or loan.

In other words, financial institutions are steadily losing the home-field advantage they once enjoyed. Instead of defaulting to existing providers, younger consumers increasingly seek recommendations from marketplaces, AI tools, and their personal networks.

Lenders and credit providers cannot ignore this. Instead of just competing against other lenders, they're competing to appear in the recommendations generated by AI assistants, comparison sites, and digital marketplaces.

Customers Quit When Effort Exceeds Value

Across every question we asked about customer experience, one pattern consistently emerged: consumers have very little patience for unnecessary effort. Whether completing an application, making a purchase, or evaluating financial offers, friction consistently reduced engagement.

The easiest way to win more customers may be eliminating those friction moments throughout the consumer credit lifecycle.

Application Abandonment

In fact, our research shows 1 in 5 consumers abandon a loan or credit card application because it asks for too much information most of the time — with 8% saying they always abandon when an application asks for too much.

For about half the time or more, this jumps to one-third of customers abandoning applications because they ask for too much. Among Gen Z consumers, the likelihood of abandoning an application half the time or more jumps to 50% when it asks for too much information.

Credit Card Convenience

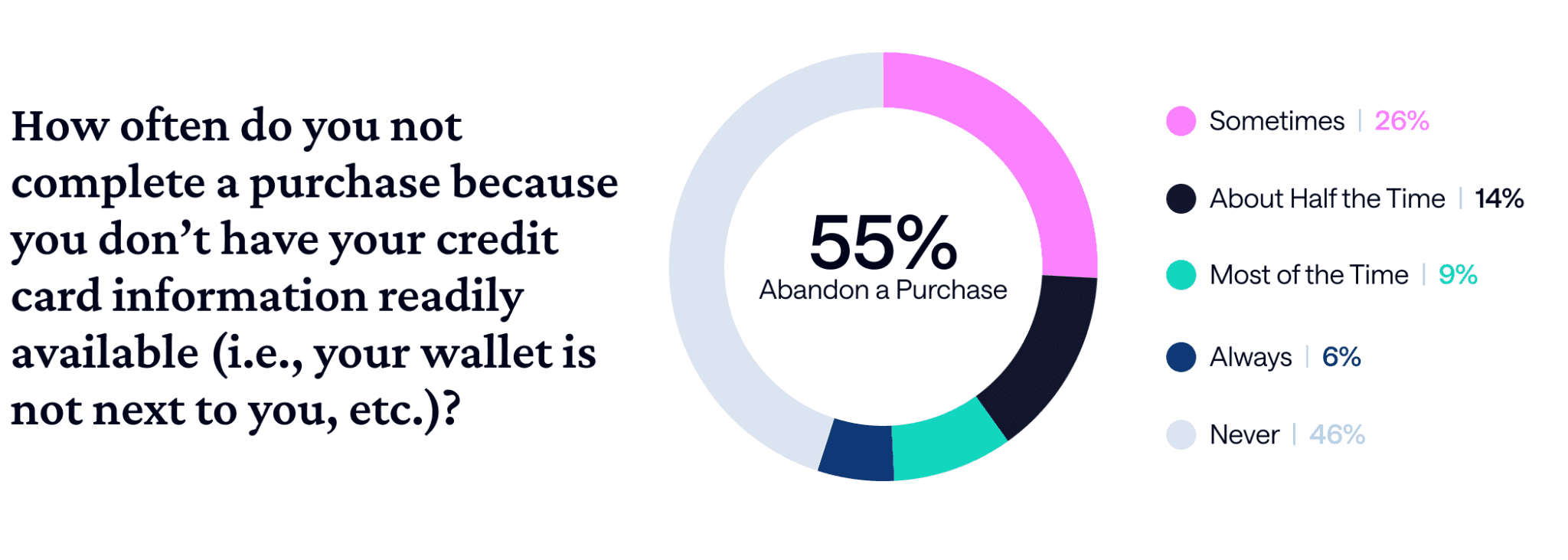

This same desire for less friction shows up in shopping carts as well. One of the biggest sources of cart abandonment is asking customers to manually type in a credit card number. Our research validates this:

This means more than 1 in 4 customers are walking away from online shopping carts about half of the time because they don’t have their card information readily available. And, Gen Z once again has less patience than other generations — 52% of Gen Z don’t complete a purchase when they don’t have their credit card information handy. That’s not just lost customers. That’s lost revenue.

Irrelevant Information

Another source of friction for consumers is simply bad information. Our research shows there is a clear opportunity to target customers with better, relevant offers that can help consumers better manage their debt. Case in point, nearly half of consumers say about half the time or more they:

Receive offers to refinance a loan or mortgage at a rate higher than they pay now (40%)

See offers for credit cards they already have (43%)

Recommending a refinance that raises someone's interest rate or advertising a credit card they already carry signals disconnected data and poor customer understanding.

Every unnecessary payment, application field, irrelevant offer, or disconnected account adds another layer of consumer friction. Institutions that systematically remove those friction points will create a measurable competitive advantage.

Five Ways to Reduce Credit Complexity for Consumers

The survey findings tell us borrowers aren't simply looking for more credit. They're looking for less complexity. That creates an opportunity for financial institutions willing to rethink how they support customers throughout the credit lifecycle.

The financial institutions and fintechs best positioned to win will focus on 5 priorities:

Develop a complete view of customer liabilities. Consumers increasingly manage debt across multiple providers. Understanding the full debt profile creates opportunities for more relevant recommendations and better customer outcomes.

Personalize recommendations using current financial data. Generic campaigns increasingly feel irrelevant. Institutions that understand what customers already owe and the credit products they have can recommend ways to actually improve their financial position.

Deliver value, not just offers. Consumers don't simply need another loan. They need help deciding which financial action makes the most sense given their existing obligations.

Reduce friction wherever possible. Every unnecessary form field, manual entry, or disconnected experience creates another opportunity for consumers to abandon the journey.

Compete beyond owned channels. As younger consumers increasingly rely on AI, marketplaces, and digital recommendations, institutions need strategies that ensure they remain visible wherever borrowing decisions begin.

Ultimately, better credit experiences mean helping consumers understand, organize, and optimize the debt they already have. Consumers need credit experiences that are easier to navigate and reduce complexity. This will do more than just improve customer satisfaction. It will earn trust, deepen relationships, and create long-term competitive advantage.

Jessica Kendall

Head of Content and Communications